Examining Public Spending—Estimates Review: A Guide for Parliamentarians

Examining Public Spending—Estimates Review: A Guide for Parliamentarians

Table of Contents

- Foreword

- 1—Roles and Responsibilities of Parliament

- 2—Government Expenditures Annual Cycle—From the Budget to the Public Accounts

- 3—The Role of Committees in Reviewing Estimates

- 4—The Office of the Auditor General’s Relationship with Parliament

- 5—Estimates-Related Questions for Standing Committees

- Appendix—Types of Votes

Foreword

The Office of the Auditor General of Canada is committed to helping parliamentarians oversee public finances. By auditing federal departments, agencies, and many other federal organizations, the Office provides Parliament with information that parliamentary committees can use to conduct hearings and make recommendations for action.

Parliamentary scrutiny of the performance of public programs is an important part of the Estimates process. Parliamentary committees play a crucial role in government accountability. Committees can challenge the government to provide clear plans and priorities and encourage departments to enhance the fairness and reliability of their performance reporting.

In the past years, concerns have been voiced in Parliament and elsewhere about the adequacy and effectiveness of committee review of the Estimates documents. It is undoubtedly a complex and laborious task. This reference document is intended to assist parliamentarians in the review process. We hope that it will be useful.

1—Roles and Responsibilities of Parliament

Parliamentary control of the public purse is fundamental to responsible government. Granting government the authority to spend is one of Parliament’s principal functions. Parliament’s power to grant this authority is founded on two basic principles:

- The government may not raise money through taxation without Parliament’s approval.

- The government may not spend money except for purposes authorized by Parliament.

These principles were already well established at the time of Confederation and were incorporated in the Constitution Act, 1867. To support parliamentary control of public money, the Constitution directs that all “duties and revenues” shall be paid into one Consolidated Revenue Fund, and all payments made from the Fund must be appropriated by Parliament.

Parliamentary authority to spend is granted through a process known as the Business of Supply. Rules governing the process are codified in the Constitution, statutes (primarily the Financial Administration Act), and the Standing Orders of the House of Commons. Grounded in centuries of parliamentary tradition, these rules are intended to ensure that parliamentarians have an adequate opportunity to scrutinize and debate the government’s spending proposals before they approve them.

The Constitution specifies that all spending measures must be initiated by the Crown—that is, the executive—and must originate in the House of Commons. In other words, it is the job of the government to prepare a spending plan and bring it to the House. The government presents this plan in the form of the Estimates.

2—Government Expenditures Annual Cycle—From the Budget to the Public Accounts

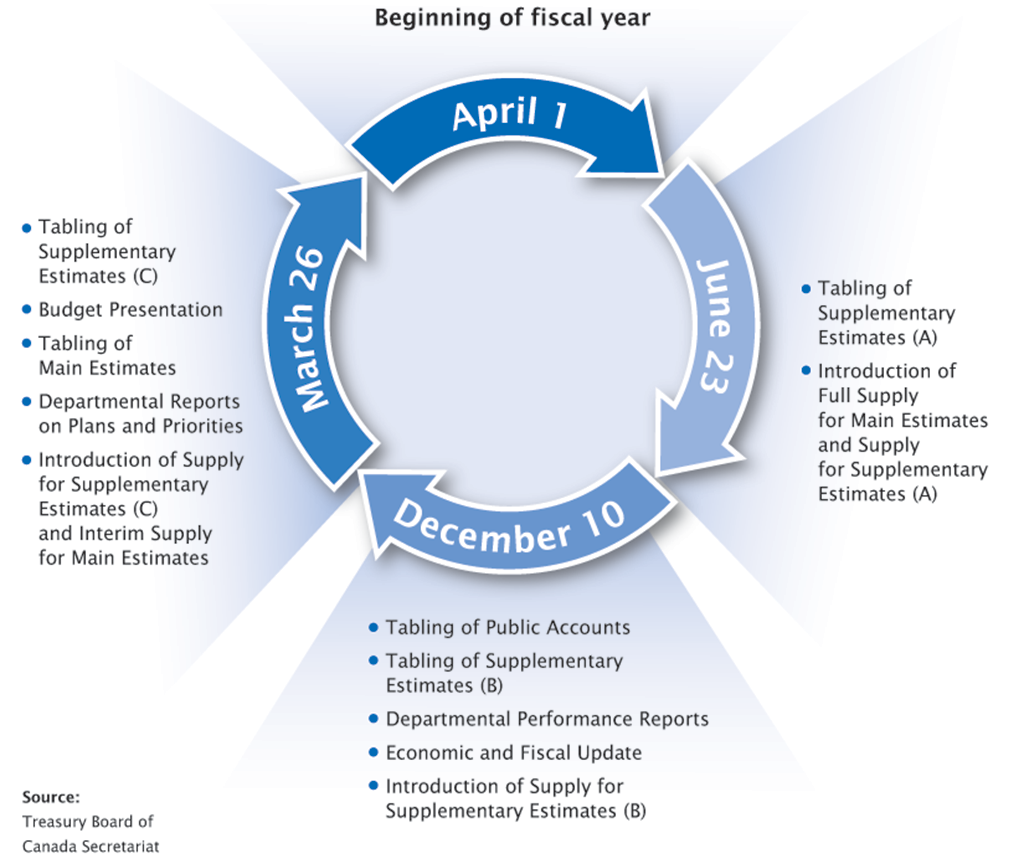

The planning and reporting of government expenditures occurs in an annual cycle that includes a specified timetable and some statutory dates. The cycle’s various elements provide the information government needs to support its development of spending plans, priority setting process, fiscal and budget decisions, and performance reporting.

The fiscal year of the Government of Canada runs from April 1 to March 31. Each fiscal year is divided into three parliamentary supply periods, a process by which the government asks Parliament to appropriate funds. Supply periods are designated by the last day that appropriation bills are generally approved by Parliament and are as follows:

- period ending June 23

- period ending December 10

- period ending March 26

Figure 1 presents the timeline of the key elements of this cycle.

Figure 1—The reporting cycle for government expenditures

Figure 1—text version

April 1

- Beginning of fiscal year

June 23

- Tabling of Supplementary Estimates (A)

- Introduction of full Supply for Main Estimates and Supply for Supplementary Estimates (A)

December 10

- Tabling of Public Accounts

- Tabling of Supplementary Estimates (B)

- Departmental Performance Reports

- Canada’s Performance

- Economic and Fiscal Update

- Introduction of Supply for Supplementary Estimates (B)

March 26

- Tabling of Supplementary Estimates (C)

- Budget Presentation

- Tabling of Main Estimates

- Departmental Reports on Plans and Priorities

- Introduction of Supply for Supplementary Estimates (C) and Interim Supply for Main Estimates

Source: Treasury Board of Canada Secretariat

The annual Budget—the government’s economic and fiscal plan

Before the beginning of the fiscal year, the Minister of Finance presents the annual Budget, usually in February or March. The Budget is a financial expression of the government’s priorities, policies, and plans. Over the past two decades, the Budget has evolved into the main vehicle for announcing new spending initiatives and tax measures. It has no legal authority, however. Although certain measures announced in the Budget may take effect immediately (for example, tax measures), spending measures must be presented for Parliament’s approval in separate legislative proposals. New spending proposals receive funding approval through the supply process, through Budget implementation acts, or through specific legislative measures, which follow the same process as other government legislative proposals.

The annual Budget includes:

- reviews of recent economic developments and the current economic outlook;

- announcements of new spending initiatives and tax changes; and

- the government’s fiscal plan, showing how much revenue the government expects to collect over its two-year planning period and medium-term horizon, how much it intends to spend, and the Debt Management Strategy.

In the fall, the Minister of Finance presents an Economic and Fiscal Update providing an update to information outlined in the Budget. Figure 2 explains how the Budget is prepared.

Figure 2—Preparing the Budget

June to October—Cabinet discussions

Cabinet holds retreats in early summer and fall to review policies, discuss priorities, and develop a Budget strategy and themes.

September to December—Pre-Budget consultations

Extensive consultations begin formally in the fall with the presentation of the Economic and Fiscal Update. The House of Commons Standing Committee on Finance then invites submissions from the public and holds hearings on priorities and issues for the upcoming Budget. It reports, with recommendations, to Parliament in December. The Minister of Finance and the Department of Finance Canada also consult with individuals, interested groups, and organizations about the forthcoming Budget.

December to February—Preparing the Budget

Drawing on these consultations and on recommendations from Cabinet policy committees, the Minister of Finance develops a proposed Budget strategy for review by the Cabinet. The Minister of Finance presents the Budget in the House of Commons, usually in February or March.

June—Budget implementation act

In some cases, spending initiatives formulated in the Budget receive legislative approval directly through a Budget implementation act, rather than through the Estimates process.

The Estimates—spending and performance documents

The Estimates documents provide a breakdown, by department and agency, of how government plans to spend public funds for the coming fiscal year. The Estimates documents have several parts.

Part I, the Government Expenditure Plan, provides an overview of federal spending and summarizes the key elements of the Main Estimates.

Part II, the Main Estimates, directly support an appropriation act. The Main Estimates identify planned government spending and the spending authorities for which the government seeks Parliament’s approval annually. Individual items in the Estimates indicate the amount of funds required by the government for particular activities or programs. The Estimates are expressed as a series of expenditures or resolutions, which summarize the estimated requirements in categories such as operations, capital, and grants and contributions. Approved expenditures are divided into categories called votes, which are set out in detail in schedules to appropriation acts. The Appendix describes the types of votes in detail.

The Estimates include statutory and non-statutory expenditures. Statutory expenditures are those that have already been authorized by previously adopted legislation; they are presented in the Estimates for information purposes only. Statutory expenditures account for about two thirds of total federal spending. Non-statutory expenditures need a specific authorization in an appropriation act.

Main Estimates support the government spending plans and are usually tabled before 1 March, followed by the Interim Supply Bill to request initial funding to cover the first three months of the new fiscal year. The Supply Bill must be approved by Parliament before April 1, and is generally approved by March 26.

The appropriation bill for the Main Estimates, called the Full Supply Bill, requests the rest of the funding for the Main Estimates, and is introduced in the House of Commons and voted on before the House adjourns in June, and is generally voted on by June 23.

Supplementary Estimates

Since the Main Estimates are tabled so closely to the government’s annual Budget, it is not always possible to include detailed Budget-related plans and priorities in the Main Estimates document. Once departments, agencies, and Crown corporations are able to provide the necessary level of detail for budget-related requirements, these and other adjustments to the spending plans are presented in subsequent Supplementary Estimates documents.

Supplementary Estimates are identified in an alphabetical sequence and are normally tabled three times a year.

- Supplementary Estimates (A) are tabled in May. The related Supply Bill to appropriate funds is introduced in the House of Commons and voted on in June.

- Supplementary Estimates (B) are tabled in late October or early November. The related Supply Bill is introduced in the House of Commons and voted on in December.

- Supplementary Estimates (C) are tabled in February, and the related Supply Bill is introduced in the House of Commons and voted on in March.

Part III, the Departmental Expenditure Plan, is divided into the reports on plans and priorities and the departmental performance reports:

- Reports on plans and priorities (RPPs) are individual expenditure plans for each department and agency (excluding Crown corporations which have corporate plans). These forward-looking reports provide information over a three-year period on an organization’s main priorities by strategic outcome, program activity, and planned or expected results, including links to related resource requirements. The RPPs also provide details on human resource requirements, major capital projects, grants and contributions, and net program costs. RPPs are usually tabled on or before March 31 of each year.

- Departmental performance reports (DPRs) are individual department and agency accounts of results achieved against planned performance expectations as set out in respective RPPs. DPRs are presented in the fall.

The Public Accounts of Canada

The Receiver General acts as the banker and as the bookkeeper for the government. As the banker, in addition to other functions, the Receiver General makes payments on behalf of departments from the Consolidated Revenue Fund. After ensuring the transactions comply with legal and policy requirements, departments send requisitions for payments to the Receiver General. Departments maintain details of the payments in departmental financial systems and balance them with Control Accounts (summarized totals) maintained by the Receiver General. Departments send summary and detailed information on payments and other transactions to the Receiver General. As the bookkeeper, the Receiver General consolidates, or rolls up, the departmental information to prepare the Public Accounts of Canada—the government’s annual report on how it has spent the funds appropriated by Parliament. This information is prepared jointly by the Receiver General for Canada (Public Works and Government Services Canada), the Treasury Board of Canada Secretariat, and the Department of Finance Canada.

The Auditor General of Canada examines the summary financial statements included in the Public Accounts to determine whether they are presented fairly in accordance with the government’s stated accounting policies, which conform to Canadian public sector accounting standards. The Auditor General’s opinion and observations are included in Volume I of the three-volume Public Accounts.

- Volume I contains the summary report and financial statements of Canada, as well as discussion and analysis of the government’s finances, including a 10-year comparison of financial data.

- Volume II presents financial operations by department.

- Volume III provides additional information and analyses such as the financial statements of revolving funds, spending on professional and special services, real estate acquisitions, transfer payments, and public debt charges.

The Public Accounts of Canada for the previous fiscal year are usually tabled by the President of the Treasury Board in the fall. By law, they must be tabled in the House of Commons within nine months of the end of the fiscal year to which they relate.

The Public Accounts of Canada are referred to the House of Commons Standing Committee on Public Accounts. The Committee reviews the federal government’s consolidated financial statements and examines financial and/or accounting shortcomings raised in the Auditor General’s observations. The Committee then makes recommendations to the government for improvements in managerial and financial practices and controls.

3—The Role of Committees in Reviewing Estimates

The House of Commons empowers its standing committees to monitor the activities of one or more departments. The committees may use their power at any time to study and report on the mandate, management, and operation of the departments assigned to them.

Standing committees of the House of Commons generally examine Main and Supplementary Estimates during supply periods. They may approve, reduce, or reject the items in the Estimates referred to them, but they may not increase the amount of a vote, change the way it is used, or redirect the funds involved. An item that has been reduced or rejected by a committee may be restored or reinstated by the House, when the appropriation bill is passed at the end of that supply period. House committees have until 31 May to review the Main Estimates and report back to the House. If they do not, the Main Estimates are deemed to have been reported, without change.

Standing committees can carry out a detailed review of Estimates by examining departments’ reports on plans and priorities and departmental performance reports and by calling ministers and department or agency officials as witnesses.

They can also hold hearings on the Auditor General’s audit reports that cover areas within their mandate. Thus, committees may become more knowledgeable about programs, providing a basis for developing recommendations on appropriate levels of spending.

After its hearings, a committee may report to the House and recommend action the government should take. Committees have the right to ask the government to respond to their recommendations in writing within 120 days.

The following are examples of committees that have specific mandates for Estimates review.

House of Commons Standing Committee on Government Operations and Estimates

The mandate of the House of Commons Standing Committee on Government Operations and Estimates consists in reviewing in particular:

- the effectiveness of government operations;

- the Estimates of departments and of central agencies (Privy Council Office, Treasury Board of Canada Secretariat, and Public Works and Government Services Canada); and

- the presentation and content of all budget documents.

This mandate reflects recommendations of the 1998 Report of the Standing Committee on Procedure and House Affairs (Catterall-Williams Report) by locating, within a single committee, broad responsibilities concerning the Estimates process and government organizations’ financial reporting to Parliament.

Committee of the Whole (House of Commons)

The Leader of the Opposition, in consultation with the leaders of the other opposition parties, selects the Estimates of no more than two departments or agencies for review by a Committee of the Whole. The chosen Estimates of each department or agency are reviewed in one sitting day.

House of Commons Standing Committee on Public Accounts

The committee examines the Public Accounts of Canada, and the reports of the Auditor General. The Committee holds hearings at which officials from both the Office of the Auditor General and audited departments appear and answer questions about the reported audit findings. The Committee focuses on government administration—the economy and efficiency of program delivery as well as the adherence to government policies, directives, and standards on administration.

Following a review, the committee reports its recommendations for government to the House of Commons with the goal of improving financial and management methods and controls of departments, agencies, or Crown corporations. The Committee seeks to hold the government to account with regard to federal spending.

Senate Standing Committee on National Finance

This committee’s field of interest is government spending that is either direct, through the Estimates, or indirect, through bills that provide borrowing authority or that pertain to the spending proposals identified in the Estimates documents. The committee also has a mandate to examine the reports of the Auditor General.

4—The Office of the Auditor General’s Relationship with Parliament

The Office of the Auditor General’s main relationship with Parliament is with the House of Commons Standing Committee on Public Accounts, because the Auditor General’s reports are automatically referred to this committee when the reports are tabled in the House of Commons. The Senate Standing Committee on National Finance also has a mandate to examine the reports of the Auditor General.

The Commissioner of the Environment and Sustainable Development’s report is reviewed by the House of Commons Standing Committee on Environment and Sustainable Development, and also periodically by the Senate Standing Committee on Energy, the Environment and Natural Resources.

There are several ways the Office can help other parliamentary committees review spending plans, past performance, and other management issues:

- Witness testimony—The Auditor General and other senior representatives of the Office are available to appear as witnesses in areas where the Office has recently done relevant audit work. Over the years, many government entities and management practices have been audited by the Office. OAG staff can describe the results of these audits to committees or to their staff. They can also comment on actions taken by departments in response to recommendations that are in the Auditor General’s reports.

- Working with committees—The Office monitors committee interests and concerns, in order to provide information that is timely and relevant. It works with committees and their staff to help them understand and efficiently use audit information.

The Office carefully considers all requests from committees to conduct audits and accepts some of them. For example, at the request of the House of Commons Standing Committee on the Status of Women, the Office carried out an audit on gender-based analysis, an analytical methodology for examining how government policies, programs, and legislation have different impacts on women and men. The findings of this audit were reported in the spring of 2009. More recently the Standing Senate Committee on Agriculture and Forestry recommended that the Commissioner of the Environment and Sustainable Development conduct a follow-up audit to its 2008 audit report on pesticides. This audit work is reported in the Commissioner’s Fall 2015 Report.

- Support to Parliament—In areas where the Office has expertise, it can provide support to parliamentarians and to individual committees on request. The Office can conduct briefings on topics of interest based on recent audit work.

5—Estimates-Related Questions for Standing Committees

This section contains lists of questions that committee members may wish to ask as the committee prepares for the planning and hearing stages of its work.

Examining program planning

- What is the program’s primary purpose?

- Are there alternative options for doing what this program does, and if so, what are their respective strengths and weaknesses?

- Is the program’s overall direction clear? Are long-term commitments spelled out? How will these be achieved?

- What key results are expected from this use of taxpayers’ funds? Do the expected results make sense in terms of the nature of the program? Is it clear what will be achieved in the short, medium and long term, by when, and at what cost?

- What key performance information will be used to track progress in achieving these results?

- Are the resources aligned with program requirements and are risks identified? How does the department explain the current level of resources allocated to the program? Would additional or fewer resources make a difference to the results, and how?

- Has middle- and long-term funding been secured and aligned with needs?

- Is the program linked to other initiatives; for example, in other departments? How will the overall efforts of the federal government on this issue be reported on? Is there a duplication of activities in the government? Does the federal program duplicate provincial programs?

- What commitments has the government or department made on program evaluation? Specifically, what evaluations are planned and when?

- Can the department achieve the same or better result with a different program, a different level of service, or a different way of delivering the existing program?

Considering program delivery issues

- Is the program sustainable in light of the risks and challenges? Have new resources been requested or authorized, and if so, what is the rationale? What actions does the new or proposed budget include that would improve results?

- Is the program financially viable in the long term? Is there a way to improve the effectiveness of the program to make its delivery less costly?

- Is there assurance that public sector values and ethics are integrated in management controls? For example, respecting codes of conduct?

- What other programs or agencies are partners in producing the desired results?

- Was the program managed with proper attention to the Public Service values of fairness and propriety?

- How has the department’s sustainable development strategy influenced the department’s key programs and activities? What has changed as a result of the sustainable development strategy?

Improving and communicating performance information

- Is the program doing what it is supposed to do? Are objectives set in expenditure plans being met? What were the results in the most recent years?

- How do the results being achieved by the program compare with those in other countries or jurisdictions? For example, how do unit costs for service delivery compare?

- Does performance information provide assurance of fairness in service delivery? For which citizen groups or regions have the results been less than desired? What is currently being done to improve deficiencies?

- Does performance information meet the committee needs? Does it provide answers to questions about the program or the department as a whole? For example, are the measures used to report results clear and reasonable? Is the evidence presented relevant and reliable?

- Could program results be delivered more effectively? What improvements are being planned for the program and are these based on objective evaluations or performance information?

- Where more than one department is involved in achieving the public policy objective, is the program’s contribution to the overall results explained well?

- How are the objectives and actions in the department’s sustainable development strategy aligned with the department’s strategic outcomes as set out in the Report on Plans and Priorities and the Departmental Performance Report?

- Has the department or agency identified lessons learned from past performance or from actions taken to address weaknesses or promote good practices?

Appendix—Types of Votes

The purpose of Estimates is to present to Parliament information in support of budgetary and non-budgetary spending authorities that will be sought through appropriation bills. These authorities are divided into two categories: voted and statutory.

Voted authorities are those for which the government seeks Parliament’s approval annually through an appropriation act. The wording and expenditure authority attributable to each vote appears in a schedule attached to the appropriation act. Once approved, the Vote wording and approved amounts become the governing conditions under which these expenditures may be made; it does not create a commitment to spend the entire amount. Individual expenditure proposals included in the Estimates and reflected in Votes seek authority to make expenditures necessary to deliver various mandates that are under the administration of a Minister and are contained in legislation approved by Parliament.

Statutory authorities are those that Parliament has approved through other legislation that sets out both the purpose of the expenditures and the terms and conditions under which they may be made. Statutory spending is included in the Estimates for information only.

Items in the Estimates are given effect through the following kinds of votes:

a) Operating Expenditures Votes—Used when there is a requirement for either a Capital Expenditures Vote or a Grants and Contributions Vote or both; that is, when spending of either type equals or exceeds $5 million. Where it does not, the appropriate items are included in the Program Expenditures Vote.

b) Capital Expenditures Votes—Used when the capital expenditures in a program equal or exceed $5 million. A Capital Expenditures Vote would include items expected to exceed $10,000 for the acquisition of land, buildings, and works (standard object 8), for acquisition of machinery and equipment (standard object 9), or for construction or creation of assets, when a department expects to draw on its own labour and materials, or when it employs consultants or other services or goods (standard objects 1 to 9). Different threshold limits may be applied for different capital expenditure classes at the departmental level.

c) Grants and Contributions Votes—Used when the grants and contributions expenditures in a program equal or exceed $5 million. Inclusion of a grant, contribution, or other transfer payment item in Main or Supplementary Estimates imposes no requirement to make a payment, nor does it give a prospective recipient any right to the funds. It should also be noted that in the vote wording, the meaning of the word “contributions” is considered to include “other transfer payments” because of the similar characteristics of each.

d) Program Expenditures Votes—Used when there is no requirement for either a separate Capital Expenditures Vote or a Grants and Contributions Vote, because neither equals or exceeds $5 million. In this case, all program spending is charged to this one vote.

e) Non-Budgetary Votes—Identified by the letter “L,” this type of vote provides authority for spending on Crown corporations, in the form of loans, advances, or investments. It also provides authority for spending, for specific purposes, on other governments, international organizations, persons, or corporations in the private sector.

f) Special Votes: Crown Corporation Deficits and Separate Legal Entities—Used when it is necessary to appropriate funds for a payment to a Crown corporation or for the expenditures of a legal entity that is part of a larger program. A legal entity for these purposes is defined as a unit of government operating under an act of Parliament and responsible directly to a Minister.

g) Special Votes: Treasury Board Centrally Financed Votes—To support the Treasury Board in performing its statutory responsibilities for managing the government’s financial, human, and material resources, a number of special authorities are required and these are outlined below.

(i) The Government Contingencies Vote supplements other appropriations. It provides the government with sufficient flexibility to meet urgent or unforeseen expenditures in cases where a valid cash requirement exists due to the timing of the payment, or where specific authority is required to make the payment (such as for the payment of grants not listed in the Estimates). The authority to supplement other appropriations lasts until Parliamentary approval can be obtained, and as long as the expenditures are within the legal mandate of the organization. The Government Contingencies Vote also serves to supplement other appropriations. It meets additional paylist costs, such as severance pay and parental benefits, which are not provided for in department Estimates.

(ii) The Government-Wide Initiatives Vote supplements other appropriations in support of the implementation of strategic management initiatives in the Public Service of Canada.

(iii) The Public Service Insurance Vote provides for the payment of the employer’s share of health, income maintenance, and life insurance premiums; for payments to or in respect of provincial health insurance plans; for provincial payroll taxes; for pension, benefit, and insurance plans for employees engaged locally outside Canada; and to return to certain employees their share of the unemployment insurance premium reduction.

(iv) The Operating Budget Carry Forward Vote supplements other appropriations for the operating budget carry forward from the previous fiscal year.

(v) The Paylist Requirements Vote supplements other appropriations for requirements related to parental and maternity allowances, entitlements on cessation of service or employment, and adjustments made to terms and conditions of service or employment of the Public Service including members of the Royal Canadian Mounted Police and the Canadian Forces, where these have not been provided from the Compensation Adjustments Vote.

(vi) The Capital Budget Carry Forward Vote supplements other appropriations for the capital budget carry forward from the previous fiscal year.

(vii) The Compensation Adjustments Vote supplements other appropriations. This vote arises as a result of adjustments made to terms and conditions of service or employment of the federal public administration (including members of the Royal Canadian Mounted Police and the Canadian Forces, Governor in Council appointees and Crown corporations as defined in section 83 of the Financial Administration Act). Departments and agencies are not required to reimburse funding allocated from this vote.